You finished the year with a profit. The accountant confirmed it. The tax bill arrived to prove it.

So why is your checking account empty?

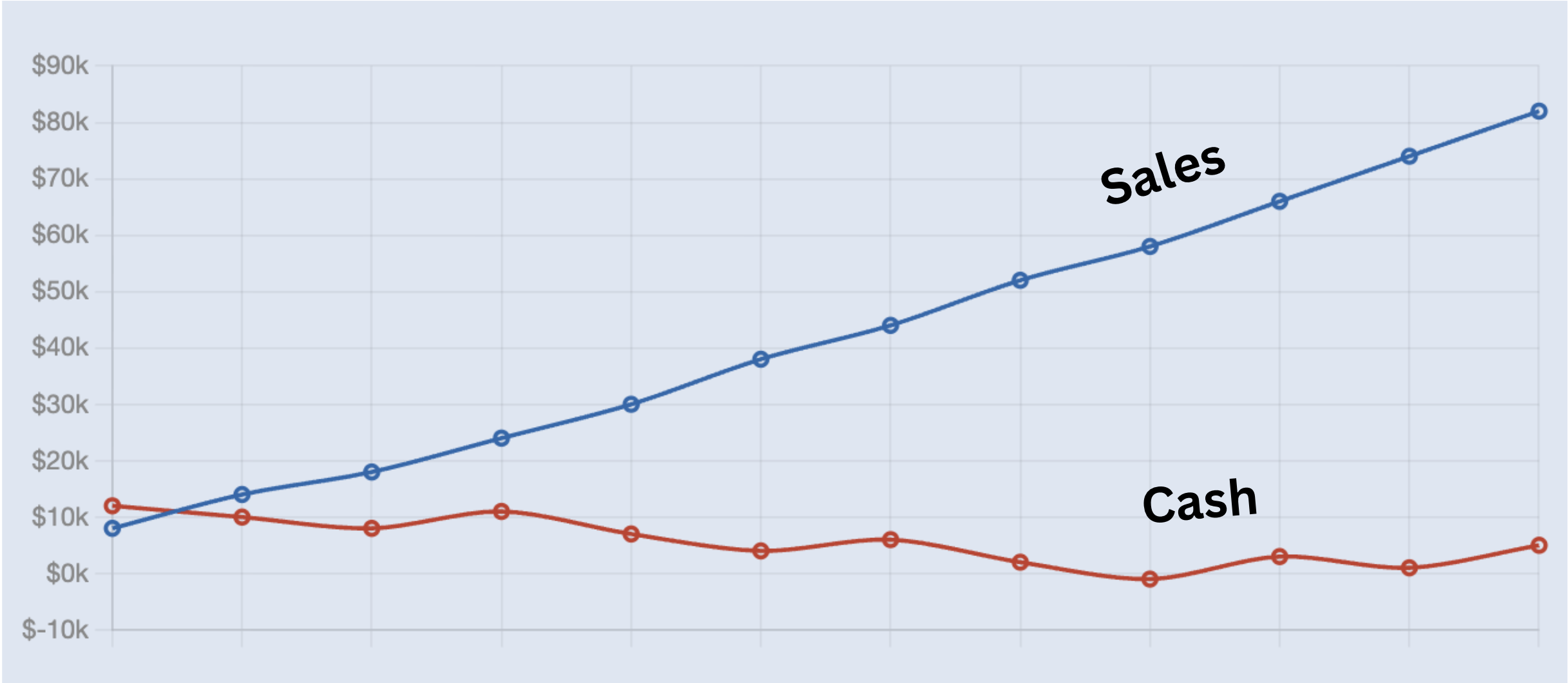

This is not an unusual question in interior design. It is, in fact, one of the most common — and most demoralizing — experiences a design firm principal can have. You did everything right. You billed your clients, you collected most of what you were owed, you watched your expenses. The numbers said you made money. And yet there's nothing there.

The explanation is simple, even if the experience of it isn't. Profit and cash are not the same thing. They are not even close cousins. Understanding why is arguably the most important financial literacy task you have as a firm owner.

The Method Behind the Confusion

There's a technical reason your P&L and your bank account tell different stories, and it has a name: accrual accounting. Your CPA almost certainly uses it, and almost certainly hasn't explained why in plain language.

Here's something your CPA will never tell you: accrual accounting was designed for public companies. The "P" in CPA stands for Public, and that's the scale of business they studied in school. It's not that accrual is wrong — it's that it was built for a different animal than a design firm doing $800,000 a year. Your CPA uses it because it's what they were taught, and because it satisfies tax and reporting requirements. What it wasn't designed to do is help you understand whether you can pay your bills next Thursday.

Under accrual accounting, transactions are recorded when they are earned or incurred — not when money actually moves. You issue an invoice, and your software records it as income immediately, whether or not your client has paid. Your vendor sends you a bill, and it becomes an expense immediately, whether or not you've paid it yet. The P&L reflects economic activity. It does not reflect cash reality. Those are two different stories, and your accounting system is only telling you one of them.

This is not wrong, exactly. Accrual accounting gives a truer picture of whether your firm is profitable on an ongoing basis, which matters for tax planning and loan applications. A good CPA can use it to manage your tax liability across years in ways that cash basis accounting doesn't allow. For those purposes, it's the right tool.

For understanding whether your firm is financially healthy on a Tuesday morning, it is nearly useless.

What Cash Actually Measures

Cash is simpler and more honest than profit. It measures one thing: what is actually in your accounts right now, available to spend.

Cash doesn't care about invoices you've issued but haven't collected. It doesn't care about revenue your accountant has recognized but your client hasn't paid. It doesn't care that you're technically profitable on paper. Cash is what you make payroll with, what you pay vendors with, what you pay yourself with.

The technical term for tracking this is cash flow — the movement of actual dollars in and out of your business over time. A firm can be profitable and cash-flow negative simultaneously. This is not a paradox. It is a timing problem, and in interior design it shows up in predictable places.

Where the Gap Opens Up

Slow-paying clients. You've earned the revenue. You've recorded the profit. Your client pays 60 or 90 days later, or disputes the invoice, or simply goes quiet. The profit was real. The cash is delayed or gone.

Procurement float. You purchase product on behalf of a client, often laying out significant sums before client reimbursement arrives. Your P&L may show this as a wash eventually, but during the float period your cash is tied up in someone else's furniture sitting in a warehouse.

Growth itself. This is the counterintuitive one. When your firm grows — more projects, more staff, more overhead — you spend cash before you earn it. You hire before the revenue arrives to justify the hire. You take on overhead to support a volume that hasn't materialized yet. Growing firms frequently show strong profits and terrible cash positions simultaneously. This is why growth without cash planning is genuinely dangerous, and why the busiest period of a firm's life is often also its most financially fragile.

Taxes on money you haven't collected. You pay tax on profit, not cash. If your profit is real but your cash is tied up in receivables or procurement float, you may owe taxes on money you haven't actually received yet. This surprises designers every single year, and it shouldn't.

The Practical Implication

Watching your P&L is necessary but not sufficient. You need a second instrument.

A basic cash flow projection — which you can maintain yourself without an accountant — tells you what's coming in, what's going out, and when. Not in accounting terms. In actual dollars, on actual dates.

A working version looks like this: list every payment you expect to receive in the next 90 days, and when. List every payment you expect to make, and when. The gap between those two columns, week by week, is your real cash position. If it goes negative at any point, you have a problem that your P&L will never show you — and that your CPA, reviewing your books quarterly, will discover long after you needed to know.

This is not sophisticated financial management. It is the minimum viable financial awareness for running a firm where money moves in irregular, project-based cycles — which describes every interior design firm that has ever existed.

One Number to Know

At any given moment you should be able to answer this question without opening your accounting software: how many weeks of operating expenses do I have in cash right now?

Not profit. Not receivables. Not what clients technically owe you. Actual cash in your accounts, divided by your average weekly overhead.

If the answer is less than four weeks, you are in a fragile position regardless of what your P&L says. If it's eight weeks or more, you have genuine operating cushion. Most designers have never calculated this number. Most designers are therefore perpetually surprised by cash crunches that were entirely predictable three months earlier.

Know the number. Update it monthly. It will tell you more about the health of your firm than any profit figure your accountant produces — and it will take you about four minutes to calculate.

Hope this helps.

David

This issue draws on Unit 6 of the Interior Design MBA Program.

Responses